With the big APRA-regulated funds now moving to the top of the list of taxpaying entities, they are realising the importance of working with their custodians to ensure after-tax investment decisions deliver for their members.

Beijing has taken some big IT strides to be a formidable challenge to the West. What is holding it back is an increasingly centralised approach to innovation, restricting the spread of new technologies that foster productivity and progress.

‘Liberation Day’ prompts abrupt repricing in global credit markets

For many months, strong fundamentals have provided a useful underpinning to credit markets, but unprecedented demand has been the key driver of spreads compressing – making valuations perilously high in some traditional market segments.

While this backdrop continued in the first quarter of 2025, trade tariff-related concerns had begun already to have an impact, with spreads widening across investment-grade and high-yield markets.

Unsurprisingly, the biggest moves in credit markets came post-quarter after President Donald Trump’s “Liberation Day” tariff announcements. Following the news, markets have been highly volatile, with credit spreads widening materially across credit asset classes.

In my opinion, concerns over the global growth outlook and uncertainty around the impact of tariffs have driven a significant repricing across credit markets, with spreads in traditional markets, such as US high yield, materially wider than at the start of the year.

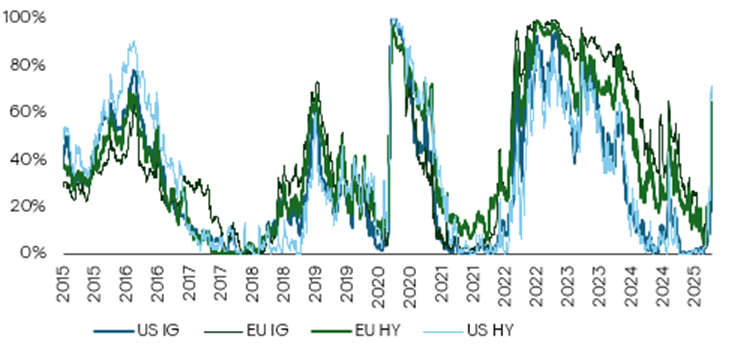

The speed of recent market moves has been remarkable. For instance, as the graph below highlights, spreads in the US high-yield market have gone from being historically tight (fifth percentile) to a more reasonable level (50th percentile).

Credit market repricing – rolling 10-year percentile of credit spreads

Source: Ninety One, ICE Indices

Forecasting the ultimate level of tariffs and quantifying their eventual impact on the global economy remains highly challenging. However, the near-term impact on the outlook for growth is unambiguously weaker, and the likely inflationary impact creates uncertainty over the outlook for monetary policy.

Companies will struggle to make decisions over investment and production in the short term, margin pressure from the tariff pass-through is uncertain, and the typical response to this uncertainty is to hire less, produce less and invest less.

Our response to this uncertain backdrop is to generally favour more defensive areas and domestically oriented sectors that are less likely to be impacted by tariffs.

In our view, it is vital to focus on issuers’ underlying credit fundamentals and their ability to withstand volatility during this period of a heightened uncertainty. Investors must be selective to ensure they limit their exposure to businesses that are likely to face a material new shock to their operating model.

More broadly, there is still a healthy degree of dispersion between asset classes, both in terms of valuations and fundamentals. Specialist areas of the credit market continue to stand out.

Bank capital (AT1s), for instance, is supported by strong fundamentals and favourable demand/supply dynamics; most banks called their AT1s in the first quarter and this theme looks set to continue given the extent to which banks have already pre-financed. Even here, though, selectivity is key.

Overall, our preference is for higher-quality components of the investment opportunity set. As risk premia start to rise, expect new opportunities to begin to emerge over the coming weeks. Certainly, we will be proactive in taking advantage of areas of the market that offer compelling risk-adjusted return potential.