The days when Australia “rode on the sheep’s back” may be long gone, but agriculture remains a critical component of the economy, generating valuable export income. While overseas investors understand its importance, for most local institutions it’s still a bridge too far.

For several years, investors, from institutional to retail, couldn’t get enough of the tech stocks with all their promises of future growth. But now the market has spoken and it’s saying precisely this – valuations matter again.

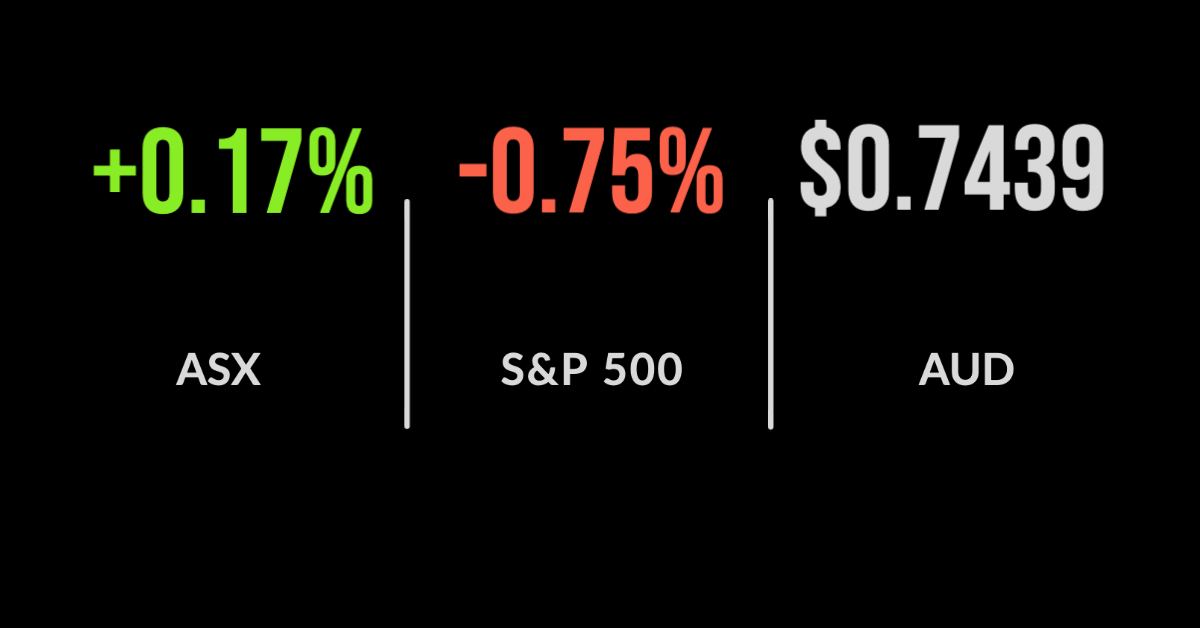

Record-setting BHP helps ASX to best week in six

ASX overcomes lockdowns, BHP, ResMed hit records, Rio Tinto’s production issues

The ASX 200 (ASX: XJO) managed a 0.2% gain on Friday even as the Delta outbreak spread across the country.

It was generally positive across the board with only the energy and utilities sectors weakening, down 0.6% and 0.4%, respectively.

The consumer discretionary and healthcare sectors were the biggest winners with investors flocking to the likes of Wesfarmers Ltd (ASX: WES) and CSL Limited (ASX: CSL) in search of defensive earnings.

Rio Tinto Limited (ASX: RIO) released production figures, announcing a 9% fall in iron ore extraction due to replacement mines, staffing issues, and higher rainfall than expected.

The miner expects unit costs of $18.00-$18.50 per tonne for the year, up from its previous estimate of $16.70-$17.70, which will have an impact on profits.

Gold miner Evolution Mining Ltd (ASX: EVN) was the biggest detractor, down 5.3%, after announcing weaker cash flow and profits than expected, whilst flagging the need for additional capital expenditure.

Both BHP Group Ltd (ASX: BHP) and ResMed (ASX: RMD) hit record highs during the week, with the former up 4.8% over the five days.

Materials were once again in focus as the Chinese central bank released the credit reins, with Fortescue Metals Group Limited (ASX: FMG) also jumping 8%.

Elsewhere, it was all about corporate activity with Australian Pharmaceutical Industries Ltd (ASX: API) adding 21.7% and Spark Infrastructure Group (ASX: SKI) increasing 21.7% and 17.4% on takeover bids.

Sell off caps negative week, investment banking reigns supreme, F45 lists

US markets weakened on Friday with the Dow Jones losing 300 points to fall 0.9% and both the S&P 500 and Nasdaq down 0.8%.

The detractors were widespread with both the energy and materials sectors taking a hit after an important sentiment index came in far weaker than expected.

Dovish comments from the Federal Reserve combined with the growing Delta outbreak have also sent bond yields below 1.3% once again.

The result was the first negative week in a month, the Dow most resilient falling just 0.5%, with the S&P 500 and Nasdaq down 1% and 1.9%, respectively, pulled down by the likes of Amazon Inc. (NYSE: AMZN).

The small-cap Russell 2000 Index, however, was the worst-performing, down 5.2% over the week, the worst since October.

The loosening of restrictions saw an unexpected jump in retail sales in June, up 0.6%, or 1.3% when volatile vehicle sales are included.

Australian-founded gym chain F45 Training is listed on the NYSE, with an eye-watering valuation of over US$2 billion.

Sticking with the Aussie theme, the James Gorman-led Morgan Stanley (NYSE: MS) delivered another near-record result, with a second-quarter profit of US$3.48 billion as investment banking revenue jumped 44% in the quarter.

This offset a similar decline in fixed income trading, with professional investors moving away from bond markets, whilst wealth management also delivered a record result.

So far 85% of S&P 500 companies have beaten expectations, the highest since 2008.

Low rates here to stay, AMP’s escape, what’s really going on

This week saw two of the most important infrastructure assets in Australia feel the heat of private equity interest, as both Sydney Airport and Spark Infrastructure saw unexpected bids.

Private equity has combined with global pension fund investors, considered by many as ‘smart money’ to buy these long-duration but interest rate sensitive assets.

History suggests that the value of these assets falls in higher interest rate environments unless they are able to pass the cost onto consumers.

The aggressive approach taken may well suggest that neither of these investors expects bond rates to go anywhere soon, and by soon that may well be several decades.

AMP’s future is becoming clearer, with ASIC indicating on Friday it would not be taking any action over the ‘fees for no service’ scandal highlighted in the Royal Commission.

It seems that whilst the events may have been lacking in morality, whether they were illegal was another question.

That said, the Royal Commission has had long-lasting impacts on the industry and seen thousands of advisers exit.

Inflation remains in the headlines every day, with the top line figures suggesting we are nearing hyperinflation, not helped by the many talking heads and hedge fund managers with strong opinions.

According to a report on Bloomberg this week, inflation is currently concentrated into components that represent just 12% of the CPI measure, when they are removed CPI increased just 0.2% not the 0.9% reported.